Debit & Credit

Debit & Credit: What’s the Difference

(and Why It Matters)

(and Why It Matters)

Credit and debit cards look nearly identical—but they work very differently. Knowing which one to use (and when) can help you avoid debt, build credit, and make smarter money moves.

Debit Cards 101

Credit Cards 101

Which Way to Pay

Debit Cards 101

Spending Your Money

A debit card pulls money directly from your checking account.

For example, if you have $200 in the bank and you spend $50, your balance becomes $150—simple. Just don’t spend more than you have!

For example, if you have $200 in the bank and you spend $50, your balance becomes $150—simple. Just don’t spend more than you have!

Pros:

- No interest charges

- Easier to avoid debt—spend only what you have

- Real-time spending tracking

- Works for in-store and online purchases

Cons:

- Doesn’t build your credit score

- Limited protection if your card is stolen

- You can’t spend more than what’s in your account (which can be good or bad)

LESSON 2

Credit Cards 101

Borrow Now, Pay Later

A credit card lets you borrow money from a bank or lender—up to a limit. You get a monthly bill and must pay back at least the minimum payment, or face interest charges (and those charges can sure add up if you aren’t careful).

Pros:

- Builds your credit score (that’s like a report card for how well grown-ups handle money)

- Stronger fraud protection than debit cards

- May offer rewards like cash back, points, or miles

- Can cover emergencies if used wisely

Cons:

- Easy to overspend

- High interest rates if you don’t pay your monthly balance in full

- Late payments = fees + credit score damage

- Misuse can lead to long-term debt

- Many credit card products include an annual fee to use

Explore debit vs. credit cards.

LESSON 3

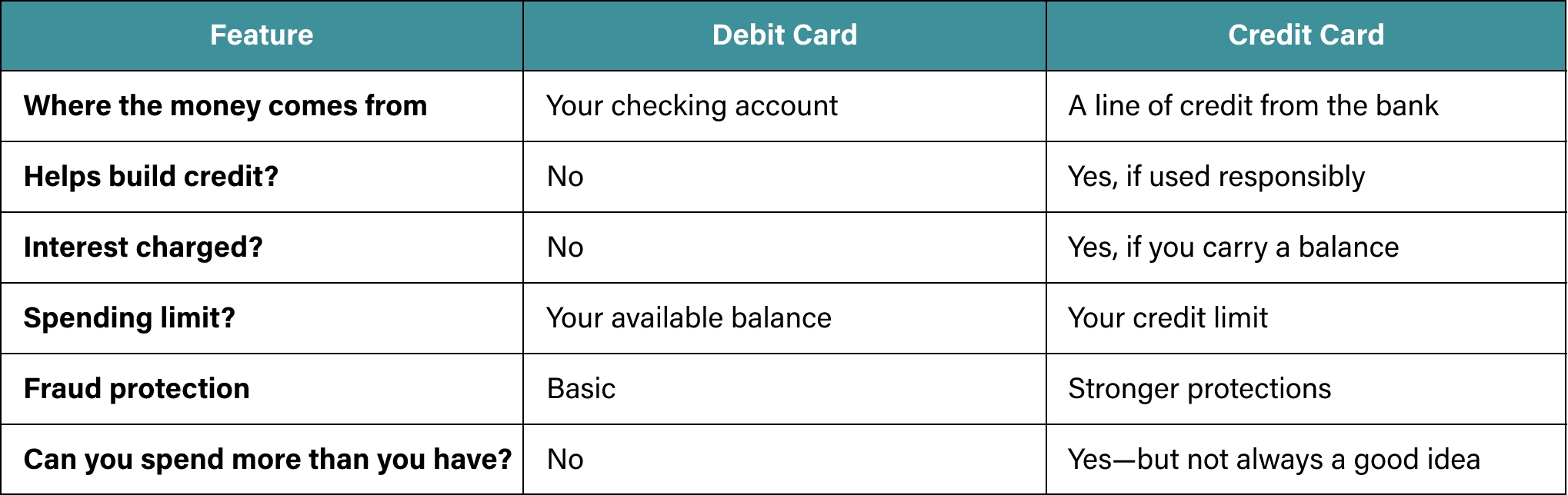

Which Way to Pay

Debit vs. Credit: A Closer Look

Let’s see what you learned.